Spare a thought for Tony Abbott now his income has fallen

Life can get tough when your income suddenly drops and doesn't the Owl know it. So spare a thought for Tony Abbott who used to have a Prime Ministerial income of $522,000, so Google tells me, but now must make do a backbencher's humble stipend of $199,040.

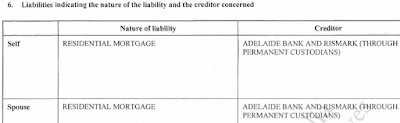

And things are really tough when you have a Sydney sized housing mortgage as the member for Warringah does. His parliamentary Statement of Registrable Instruments indicates the following:

Which might be troubling for him if that Rismark association is anything to do with the matters described in this Shared equity loans expensive way to buy story that appeared on news.com.au website back in 2009

And things are really tough when you have a Sydney sized housing mortgage as the member for Warringah does. His parliamentary Statement of Registrable Instruments indicates the following:

Which might be troubling for him if that Rismark association is anything to do with the matters described in this Shared equity loans expensive way to buy story that appeared on news.com.au website back in 2009

THE new shared equity mortgage allows borrowers to buy property they traditionally couldn't afford – but this privilege isn't cheap, particularly if house prices jump.

The new product has sparked fears it will add to the growth in house prices because of the extra flow of liquidity to the market.

The loan has been launched as an equity finance mortgage (EFM) and is issued by Adelaide Bank and funded by Rismark International.

Brian Jones, managing director of non-bank lender Homeloans, which recently wrote the country's first EFM loan in Perth, said the product was designed to overcome poor home affordability in NSW and Victoria.

“It's had that original foundation in that there was a problem with, particularly younger people and affordability in high-value markets, possibly having to move away from family and look for employment elsewhere rather than having free access to the markets and the geography that they were accustomed to,” he said.

“This is the perfect product for borrowers who want to buy a property but keep monthly repayments to a minimum.”

Aspirational homebuyers taking out an EFM are able to borrow up to 25 per cent more than normal, giving first homebuyers the ability to break into the housing market.

The EFM loan is taken in conjunction with a standard mortgage.

While borrowers pay interest on the standard mortgage, there is no interest payable and no monthly repayments on the EFM portion of the loan.

Instead, borrowers pay the lender up to 40 per cent of the capital appreciation of the house at the end of the term.

The idea behind the EFM works – homebuyers can choose to buy a more expensive property rather than move to a cheaper area, while keeping their monthly repayments low.

However, borrowers need to understand that this strategy costs more in the long-term.

Comments